As most of higher education is concerned about their financial position, a growing number of colleges are trying to encourage academic units to generate additional revenues and cut back on expenses. One popular way of doing this is through responsibility center management (RCM) budget models, which base a portion of a unit’s budget on their ability to effectively generate and use resources.[1]

Both universities that I have worked at (Seton Hall and Tennessee) have adopted variations of RCM budget models, and there is a lot of interest—primarily at research universities—in pursuing RCM. Having been through RCM, I am quite interested in the downstream implications of RCM on how leaders of institutions and units behave. There are a couple of good scholarly articles about the effects of RCM that I use when I teach higher education finance, but they are based on a small number of fairly early adopters and the findings are mixed.

One of my current research projects is examining the growth of master’s degree programs (see our recent policy brief), and I have a strong suspicion that institutions adopting RCM budget models are more likely to launch new programs as units try to gain additional revenue. My sense is that there have been a lot of recent adopters, but the best information out there about who has adopted RCM comes from slides or information provided by consulting firms (which often are not under contract by the time the model is supposed to be fully implemented). This led me to spot check a few institutions commonly listed on charts, and some of them appear to have either never gotten past the planning stage or quietly moved to another budget model.

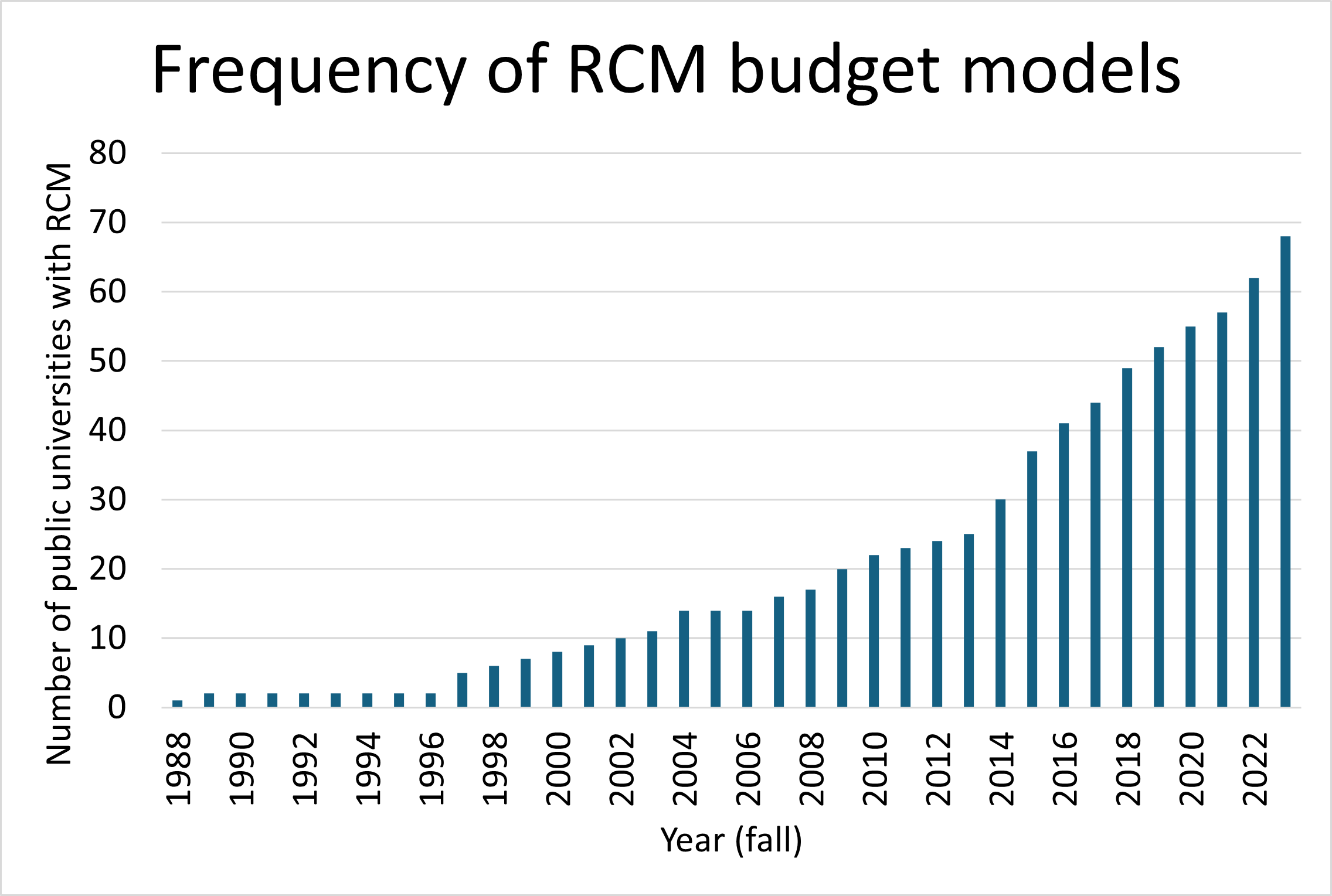

My outstanding research assistant Faith Barrett and I went through documents from 535 public universities (documents from private colleges are rarely available) to collect information on whether they had announced a move to RCM, actually implemented it, and/or abandoned RCM to return to a centralized budget model.[2] The below figure summarizes the number of public universities that had active, implemented RCM budget models for each year between 1988 and 2023.[3]

There has been a clear and steady uptick in the number of public universities with active RCM models, reaching 68 by 2023. Most of this increase has happened since 2013, when just 25 universities used RCM. Only seven universities that fully implemented RCM fully abandoned the model based on publicly available documents (Central Michigan, Ohio, Texas Tech, Illinois-Chicago, Oregon, and South Dakota), although quite a few colleges have backed off how much money flows through RCM.

Additionally, a number of universities publicly announced plans to move to RCM before apparently abandoning them before implementation. Some examples include Missouri, Nebraska, and Wayne State. This is notable because these are often included on consultants’ slide decks as successful moves to RCM.

Here is the list of universities that had fully implemented RCM by fall 2023. If you see any omissions or errors, please let me know!

| Name | State |

| Auburn University | AL |

| University of Alabama at Birmingham | AL |

| University of Arizona | AZ |

| University of California-Davis | CA |

| University of California-Los Angeles | CA |

| University of California-Riverside | CA |

| University of Colorado Boulder | CO |

| University of Colorado Denver/Anschutz Medical Campus | CO |

| University of Delaware | DE |

| University of Central Florida | FL |

| University of Florida | FL |

| Georgia Institute of Technology-Main Campus | GA |

| Iowa State University | IA |

| University of Iowa | IA |

| Boise State University | ID |

| Idaho State University | ID |

| University of Idaho | ID |

| University of Illinois Chicago | IL |

| University of Illinois Urbana-Champaign | IL |

| Ball State University | IN |

| Indiana University-Bloomington | IN |

| Indiana University-Purdue University-Indianapolis | IN |

| Kansas State University | KS |

| University of Kansas | KS |

| Northern Kentucky University | KY |

| Western Kentucky University | KY |

| University of Baltimore | MD |

| University of Michigan-Ann Arbor | MI |

| University of Michigan-Dearborn | MI |

| Western Michigan University | MI |

| University of Minnesota-Twin Cities | MN |

| University of Missouri-Kansas City | MO |

| The University of Montana | MT |

| North Dakota State University-Main Campus | ND |

| University of North Dakota | ND |

| University of New Hampshire-Main Campus | NH |

| Rutgers University-Camden | NJ |

| Rutgers University-New Brunswick | NJ |

| Rutgers University-Newark | NJ |

| University of New Mexico-Main Campus | NM |

| Kent State University at Kent | OH |

| Miami University-Hamilton | OH |

| Miami University-Middletown | OH |

| Miami University-Oxford | OH |

| Ohio State University-Main Campus | OH |

| University of Cincinnati-Main Campus | OH |

| Oregon State University | OR |

| Southern Oregon University | OR |

| Pennsylvania State University-Main Campus | PA |

| Temple University | PA |

| University of Pittsburgh-Pittsburgh Campus | PA |

| College of Charleston | SC |

| University of South Carolina-Columbia | SC |

| East Tennessee State University | TN |

| Tennessee Technological University | TN |

| The University of Tennessee-Knoxville | TN |

| University of Memphis | TN |

| The University of Texas at Arlington | TX |

| The University of Texas at San Antonio | TX |

| University of Utah | UT |

| George Mason University | VA |

| University of Virginia-Main Campus | VA |

| Virginia Commonwealth University | VA |

| University of Vermont | VT |

| Central Washington University | WA |

| University of Washington-Bothell Campus | WA |

| University of Washington-Seattle Campus | WA |

| University of Wisconsin-Madison | WI |

[1] This is also called responsibility centered management, and I cannot for the life of me figure out which one is preferred. To-may-to, to-mah-to…

[2] RCM can be designed with various levels of centralization. Pay attention to the effective tax rates that units pay to central administration—they say a lot about the incentives given to units.

[3] This excludes so-called “shadow years” in which the model was used for planning purposes but the existing budget model was used to allocate resources.

Your list looks quite complete. I believe due to budgetary challenges, the Arizona Board of Regents mandated that U of Arizona cease using its RCM budget model and told ASU and NAU that they could not use such a model. See https://www.azregents.edu/sites/default/files/2024-02/Arizona_Board_of_Regents-Enhanced_Financial_Oversight_Report-February_9_2024.pdf

Your list looks accurate based on my experience in the field and complete. The exception would be the University of Arizona as the AZ Board of Regents mandated a model change due to recent financial difficulties. See: https://www.azregents.edu/sites/default/files/2024-02/Arizona_Board_of_Regents-Enhanced_Financial_Oversight_Report-February_9_2024.pdf

Thank you for sharing that. I appreciate it!