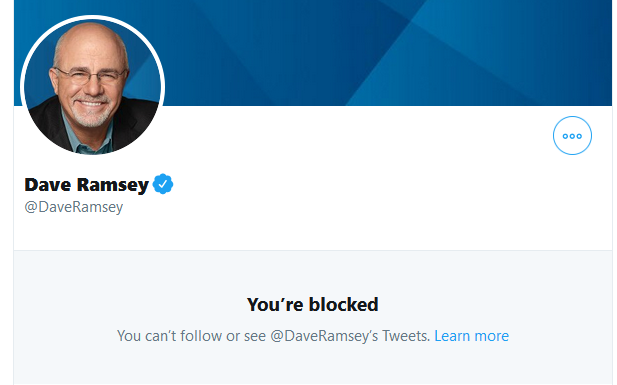

Well-known personal finance personality Dave Ramsey apparently tweeted out something about paying for college yesterday. When I went to click on the link, I got the following notice from Twitter.

As far as I am aware, this is the first time that someone has blocked me on Twitter (I only use the blocking function for likely Russian bots and people who have made racist or sexist statements against people I know). And I’m pretty sure I know the reason why Ramsey blocked me—this interview that I did with Money magazine last spring in which I noted that his advice to avoid all college debt is a generally bad idea for students. Limiting ridiculous credit card debt and having a plan to pay off debt eventually are sound recommendations, but delaying the labor market benefits of a college credential to work your way through debt-free just doesn’t make long-term sense for most people. (And research shows that borrowing for college can improve student outcomes.)

As far as I am aware, this is the first time that someone has blocked me on Twitter (I only use the blocking function for likely Russian bots and people who have made racist or sexist statements against people I know). And I’m pretty sure I know the reason why Ramsey blocked me—this interview that I did with Money magazine last spring in which I noted that his advice to avoid all college debt is a generally bad idea for students. Limiting ridiculous credit card debt and having a plan to pay off debt eventually are sound recommendations, but delaying the labor market benefits of a college credential to work your way through debt-free just doesn’t make long-term sense for most people. (And research shows that borrowing for college can improve student outcomes.)

On the other hand, students also should be reasonable about how much they borrow for college. While I was pulling up the Money magazine link for the previous paragraph, I noticed that their feature piece today is on someone with $185,000 in student loan debt and who is struggling to make minimum payments. There are key details missing in the piece, such as how much of the debt is for graduate school, the person’s income, and how much interest has capitalized, but this is certainly a cause for concern absent additional information (which seems to be missing from many of these pieces).

So this brings me to a question that I get asked quite a bit: how much should students borrow for college? To me, the correct answer is generally “it depends”—but most people don’t like that classic answer from a tenured professor. This leads me to specify some basic ground rules that students and their families should consider before signing that Master Promissory Note.

For undergraduate students: I am generally not concerned if students take out the maximum amount in federal student loans in their own name while in college. Younger (dependent) students can typically take out up to $31,000 in federal loans, while independent students can take out up to $57,500. These loans have generous income-driven repayment options that reduce payments if college doesn’t work out financially for a student. (Any forgiven balance outside of Public Service Loan Forgiveness may be taxed, but my guess is that Congress patches that fix on an annual basis going forward.)

Beyond that amount, students and their families may be able to get Parent PLUS or private loans, which generally require a co-signer and varied levels of creditworthiness in order to qualify. Parent PLUS loans scare me (as I talked about last fall with NPR), as they require many parents to pay loans into their retirement and have much lower credit standards than private loans. Students and their families need to have long and hard conversations about borrowing beyond the federal student loan limit to see if parents or co-signers can afford to repay those loans and the student’s likely ability to help parents repay those debts.

For graduate students: Most six-figure student debt burdens are from graduate school, since students can borrow up to the full cost of attendance in their own name through the Grad PLUS program and many of these programs tend to be expensive. New program-level College Scorecard data show that a large number of master’s and professional doctorate programs graduate students with more than $100,000 in debt. And I can speak to this personally as my wife and I are down to the final year of payments on her $110,000 in law school debt.

Income-driven repayment plans and PSLF extend to all graduate debt through the federal government, so there is some protection against low earnings after attending graduate school. However, unless a student is sure that he or she is going to be in a public service field and receive PSLF, it is important to keep loan balances in mind. Income-driven repayment plans require 20 years of payments instead of the ten years under PSLF, and this requires committing ten percent of your income over 150% of the poverty line for much of your prime earning years. Sit down with your family and try to get a handle on expected future earnings (program-level earnings data will come out this fall) and other expenses such as childcare and housing and see what is affordable. $100,000 in debt is extremely manageable for a two-income household making $150,000 per year, but much harder for a single adult making $60,000 per year.

The right answer for how much a student should borrow for college depends quite a bit on individual circumstances, but in general the modest federal loan limits for undergraduate students are manageable for most graduates with the help of income-driven repayment programs. Dave Ramsey may be an influential voice in the personal finance world, but following all of his advice on paying for college is likely to be a losing proposition for many students.

Informative and well written. Amusing that you were blocked for making a good case for reasonable borrowing.