The concept of risk sharing, in which colleges are held at least partially financially responsible for the outcomes of their students, has become a hot topic of political discussion in recent months. The idea has gained bipartisan support–in least in theory–as presidential candidates Hillary Clinton and Scott Walker have both supported the basic principles of risk sharing. Yet by potentially penalizing colleges with high student loan default rates, risk sharing systems have the incentive to reduce access to higher education while not actually incentivizing colleges to improve.

With generous support from the Lumina Foundation, I set out to sketch out a risk sharing system with the goal of increasing accountability for poor outcomes while recognizing differences in the types of students colleges serve. I released the resulting paper this week and testified in front of the U.S. Department of Education’s Advisory Committee on Student Financial Assistance on the topic. (My testimony is below.) I welcome your comments on risk sharing, as the goal of this paper and testimony is to advance a thoughtful conversation on what a fair and effective system could look like.

For more reading on risk sharing, I highly recommend the thoughtful takes of the American Enterprise Institute’s Andrew Kelly and Temple University’s Doug Webber.

Testimony to the Advisory Committee on Student Financial Assistance

Hearing on Higher Education Act Reauthorization

Robert Kelchen

Good afternoon, members of the Advisory Committee on Student Financial Assistance, Department of Education officials, and other guests. My name is Robert Kelchen and I am an assistant professor in the Department of Education Leadership, Management and Policy at Seton Hall University. All opinions expressed in this testimony are my own, and I thank the Committee for the opportunity to present.

My testimony today will be on the topic of risk sharing in higher education, which is typically defined as holding colleges financially accountable for their students’ performance. It is a topic that has been discussed by politicians on both sides of the aisle, including legislation recently introduced by Republican Senator Orrin Hatch and Democratic Senator Jeanne Shaheen that would require colleges to pay a percentage of students’ loans that were not paid on in the previous year.[1] But simple risk sharing proposals like this provide colleges with incentives to reduce borrowing by either leaving the Direct Loan program or reducing non-tuition expense allowances included in the cost of attendance.

In a recently-released policy paper funded by the Lumina Foundation, I introduced a risk sharing proposal that attempts to hold colleges accountable for their performance with respect to both Pell Grant and federal student loan dollars.[2] My proposal would reward colleges for strong performance on Pell Grant success and student loan repayment rates, while requiring colleges with weaker performance to pay a penalty to the Department of Education from a source other than institutional aid dollars.

The federal government’s portion of my proposed risk-sharing system would have three main components:

- First, penalties or rewards for Pell Grant recipients’ performances would be separate from penalties or rewards for student loan performance. This would end the current situation in which colleges face incentives to opt out of federal student loans in order to protect Pell Grant dollars.[3]

- Second, the federal government would provide better tracking and reporting of outcomes for students receiving federal financial aid. The set of metrics available to examine performance is extremely limited, and could be improved by either overturning the ban on federal student unit record data systems or committing to providing additional subgroup performance information using IPEDS and the National Student Loan Data System.

- Third, in order to make more accurate comparisons about student loan performance across campuses, federal guidelines for how the non-tuition components of the cost of attendance are defined would be helpful. Research has found large variations in the off-campus room and board and other expense allowances, which are determined by individual colleges, within a given metropolitan area.[4] Colleges need to be placed on a more level playing field for accountability purposes.

Colleges would be required to meet three criteria to receive Title IV funds:

- First, colleges must agree to put “skin in the game” by being willing to match a percentage of Title IV loan or grant aid with institutional funds if their performance falls below a specified benchmark.

- Second, colleges must participate in the Federal Direct Loan program in order for their students to receive Pell Grant dollars, giving students access to credit while not directly putting Pell dollars at risk.

- Third, colleges must be willing to meet heightened accreditation and consumer information provision standards.

Colleges’ performance would be compared to similar institutions using peer groups based on the characteristics of students served, types of degrees and certificates offered, and the level of resources different colleges possess. Notably, by using institutional selectivity, per-student revenues, and endowment values as grouping characteristics, a college would be compared to more selective colleges if it tried to become more selective—limiting its ability to game the system.

The Pell Grant portion of risk sharing would be based on outcomes such as Pell recipients’ retention rates, graduation rates, transfer rates, and the number of graduates. Colleges with performance a certain percentage below the peer group average would have to pay a penalty equal to a percentage of Pell funds awarded out of their own budget, while colleges a certain percentage above the average would receive a bonus to use to supplement need-based financial aid programs.

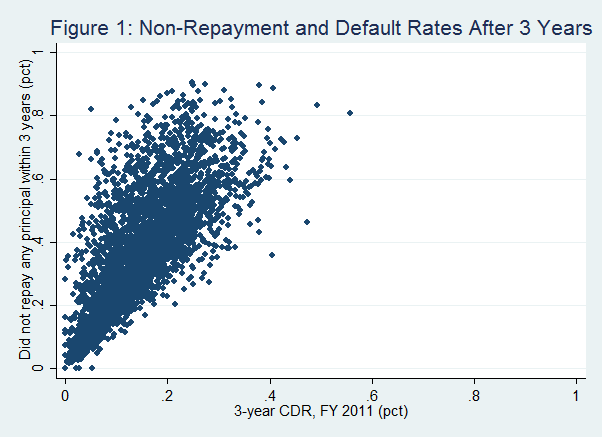

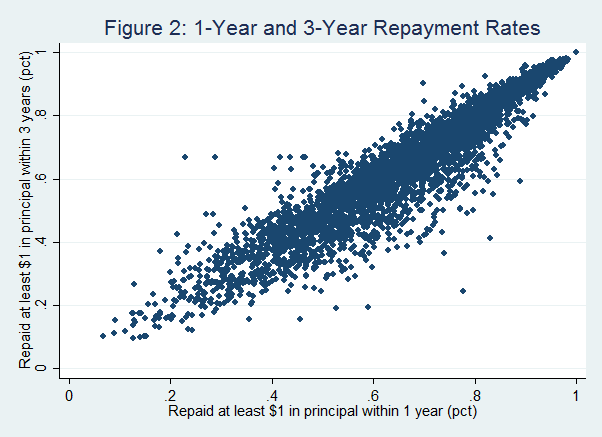

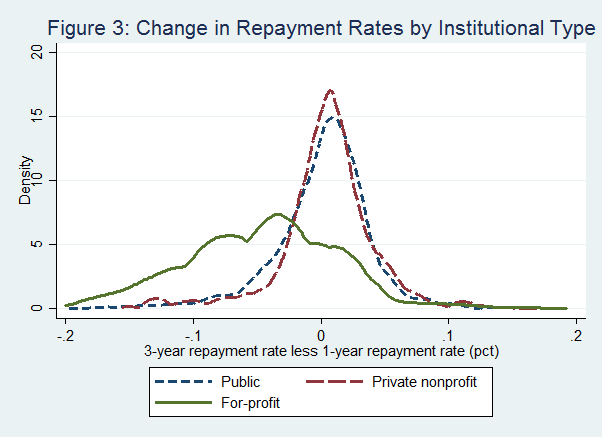

The student loan portion of risk sharing would be based on outcomes such as cohort default rates 3-5 years after entering repayment, the percent of students current on their payments, and the percentage of students making payments of at least $1 of principal. I would also include PLUS loans in the risk sharing metric. Colleges performing substantially above the peer group average would get additional work-study funds, while colleges performing substantially below average would face a penalty.

The implementation of any risk sharing proposal must be carefully considered in order to avoid perverse incentives and to gain support from colleges and policymakers. Lessons from state performance-based funding program show that implementing over a period of several years is important, as is some method for colleges to limit penalties until they can change their organization.[5] Colleges that can present clear plans for improvement that are supported by their accreditor should be able to get reduced penalties and logistical support from the federal government for a limited period of time.

Thank you once again for the opportunity to present and I look forward to answering any questions.

[1] Student Protection and Success Act (S. 1939, introduced August 5, 2015). http://www.shaheen.senate.gov/imo/media/doc/Student%20Protection%20and%20Sucess%20Act.pdf.

[2] The paper is available at http://www.luminafoundation.org/resources/proposing-a-federal-risk-sharing-policy.

[3] Hillman, N. W. (2015). Cohort default rates: Predicting the probability of federal sanctions. Educational Policy, 29(4), 559-582. Hillman, N. W., & Jaquette, O. (2014). Opting out of federal student loan programs: Examining the community college sector. Paper presented at the Association for Education Finance and Policy annual conference, San Antonio, TX.

[4] Kelchen, R., Hosch, B. J., & Goldrick-Rab, S. (2014). The costs of college attendance: Trends, variation, and accuracy in institutional living cost allowances. Madison, WI: Wisconsin HOPE Lab.

[5] For example, see Dougherty, K. J., & Natow, R. S. (2015). The politics of performance-based funding: Origins, discontinuations, and transformations. Baltimore, MD: Johns Hopkins Press.