The topic of college closures has gotten even more attention since the beginning of the coronavirus pandemic last spring. Even though the number of private nonprofit colleges closing remained around recent norms in 2020 (approximately ten degree-granting institutions), many colleges have absorbed sizable losses during the pandemic and will continue to do so in coming years. In a recent working paper that I wrote with Dubravka Ritter of the Federal Reserve Bank of Philadelphia and Doug Webber of Temple University, we estimate that colleges and universities may lose approximately $100 billion in revenue over the next five years. This means that colleges are still going to face financial challenges going forward.

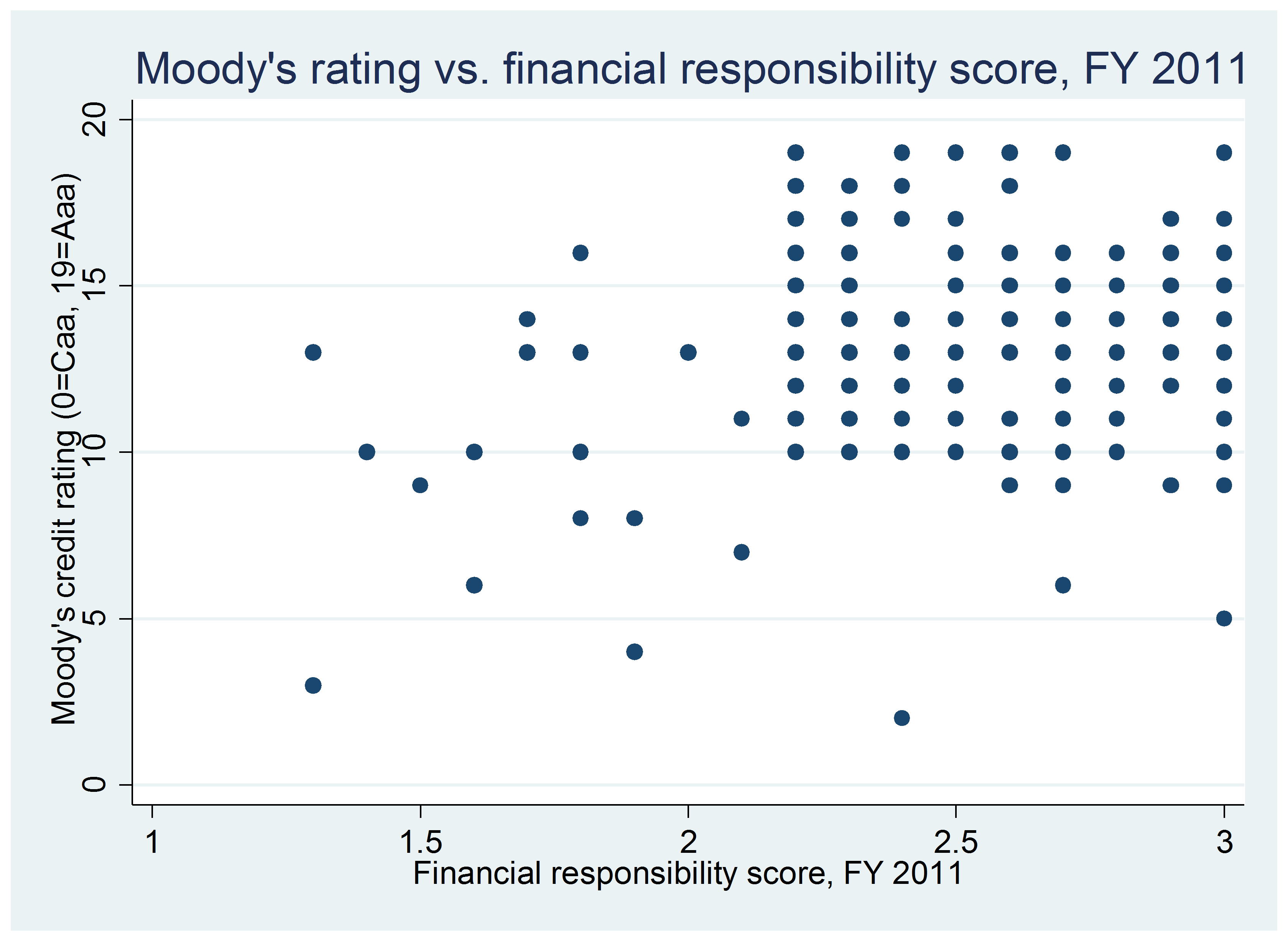

One of the federal government’s main tools to identify colleges at risk of closure is financial responsibility scores. Private nonprofit and for-profit colleges are scored on a scale of -1.0 to 3.0 based on three measures: a primary reserve ratio, a net income ratio, and an equity ratio. Colleges that score at 1.5 or above pass, while colleges that score between 1.0 and 1.4 are in an oversight zone and colleges that score at 0.9 or below fail. Colleges that fail must submit a letter of credit in order to keep receiving federal financial aid, and colleges that are in the oversight zone or fail are subject to additional financial monitoring.

The financial responsibility scores for fiscal years ending in 2018-19 were recently released by Federal Student Aid, and this represents the final pre-pandemic look at colleges’ finances. The distribution of listed scores by sector is below. The vast majority of colleges in both sectors passed, but a larger number of for-profit colleges failed than in the private nonprofit sector.

| Outcome | For-profit | Nonprofit |

| Pass | 1,517 | 1,479 |

| Zone | 51 | 51 |

| Fail | 123 | 49 |

| Total | 1,691 | 1,579 |

Four years ago, I looked at the financial responsibility scores of private nonprofit colleges that closed in 2016. Of the 12 colleges with available data, four colleges passed, two were in the oversight zone, three failed, and the final three institutions were placed on heightened cash monitoring for financial responsibility score issues without assigning a score.

I repeated this exercise for twelve private nonprofit colleges that closed or merged in 2020 or 2021 and had available data. As shown below, not a single college that closed received a failing financial responsibility score. Three were in the oversight zone, three were instead placed on heightened cash monitoring for financial responsibility concerns, and the other six all passed. Holy Family College in Wisconsin, which closed in 2020, had a perfect score.

| Name | Financial responsibility score |

| Judson College | 2.1 (pass) |

| Becker College | Placed on HCM1 |

| Concordia College (NY) | Placed on HCM1 |

| Marlboro College | 1.8 (pass) |

| Wesley College (DE) | Placed on HCM1 |

| Pine Manor College | 1.0 (zone) |

| Holy Family College (WI) | 3.0 (pass) |

| Urbana University | 2.9 (pass) |

| MacMurray College | 2.6 (pass) |

| Robert Morris University (IL) | 1.3 (zone) |

| Concordia University (OR) | 1.1 (zone) |

| Watkins College of Art | 2.2 (pass) |

Next year’s release of financial responsibility scores will begin to show the effects of the pandemic at colleges which had their fiscal years end after the pandemic began. The 2020-21 IPEDS data collection cycle also includes for the first time values for each component of the financial responsibility score so analysts have more information about colleges’ financial positions.