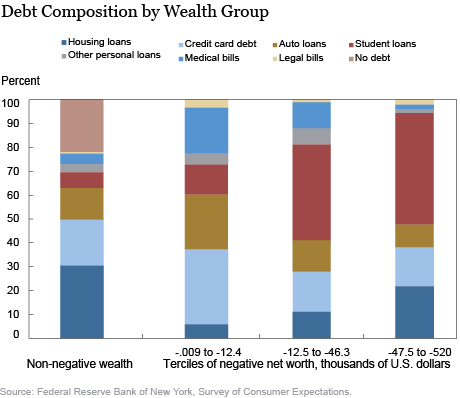

A recent analysis by economists at the Federal Reserve Bank of New York looked at the approximately 14% of American households that had negative wealth in 2015 and pointed out student loan debt as a key driver of negative wealth. As a key figure from the report (which is reprinted below) shows, student loan debt is responsible for between 40% and 50% of total negative wealth among households with a net worth of below -$12,500.

This isn’t a tremendously surprising finding, although it’s always helpful to document something intuitive with actual data (although self-reported data always come with caveats). Student loans are one of the few types of debt aside from medical or legal bills that can be taken on in large amounts without having outstanding credit or collateral. Credit card debt is another way to take on debt, but most people with negative wealth won’t be able to access large lines of credit this way. It’s also possible to be underwater on a house (by owing more than its current value), but this affects a relatively small percentage of households.

The authors of the analysis then wrote the following about the implications of student loan debt:

“It is likely that the steady growth in student debt and borrowing, combined with the very slow rate of student loan repayment we have documented elsewhere, has materially contributed and will continue to contribute to negative household wealth and wealth inequality.”

As I told Inside Higher Ed in their summary of the analysis, I only partially agree with that assessment. The challenge with this analysis is that it combines students who completed and did not complete a degree (likely due to sample size issues, as the dataset includes questions about educational attainment). As the authors note, households with a bachelor’s degree or higher and negative net worth tend to have a young head of household. For example, my household is just now leaving negative net worth territory, five years after our head of household completed law school.1 Paying off student loan debt is difficult, but the rapid growth in takeup of income-driven repayment plans among high-debt individuals (as shown in this recent White House report and in the chart below) has the potential to reduce this burden.

I’m far more concerned about the implications for wealth inequality among students who did not complete a degree and are unaware of income-driven repayment options. Although there are positive economic returns on average for students who attend college but do not graduate, they are far smaller than students who finish. A better measure of wealth inequality would look at how wealth progresses over a ten-year window after a student leaves college. If he or she is able to repay loans and build assets, the picture is far less bleak than if a student still has negative wealth due to student loans and other types of debt.

———————————————————————————————————

1 In 2016, the term “head of household” is outdated. In households where both adults work, it’s far from clear who should be the head and who isn’t. It would be better to know the highest educational attainment of either of the adults.