The traditional way to repay federal student loans was for students to pay back their loans over a ten-year period of time, generally by making the same payment each month. But as student loan debt has generally risen over time (although falling ever so slightly in the most recent quarter), paying off larger loans in a short period of time has become more difficult for many borrowers. This has made income-driven repayment plans, expanded during both the Bush and Obama Administrations, an appealing option for more students (although the future price tag of the programs is something to watch closely in the future).

The U.S. Department of Education recently released new data (updated every three months) on the federal student loan portfolio showing the growth in income-driven plans. The chart below shows the percentage of dollars in the Direct Loan program that are in one of four broad categories: 10-year payment plans not tied to income, longer payment plans not tied to income, income-driven plans, and miscellaneous plans that don’t fit well in any of the above three categories.1

Since 2013 (when repayment plan data first became available), the federal government’s holdings in the Direct Loan program have risen from $361 billion to $673 billion. The amount of loans in the standard ten-year repayment plan rose from $168 billion to $267 billion during this time, but the amount in income-driven plans rose from $72 billion to $269 billion in just three years. Income-driven plans now make up 40.0% of all Direct Loan dollars, while 39.7% of dollars are now in ten-year plans.

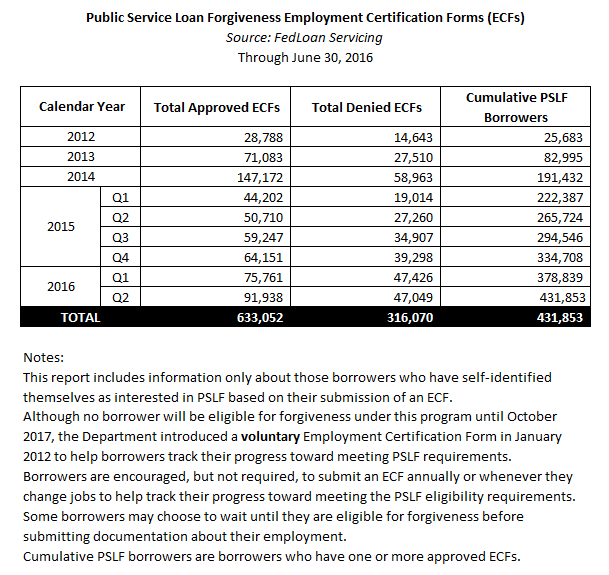

The Department of Education also released data for the first time on the number of students seeking employment certification in the Public Service Loan Forgiveness (PSLF) program, which will allow students working in approved fields to make ten years of payments instead of 20-25 years under other income-driven plans. While students aren’t officially in PSLF until they complete ten years of payments (the first students will do so in October 2017), this is an interesting measure of potential interest in PSLF. The below figure (from Federal Student Aid) shows the number of students who have submitted employment certification forms in possible preparation for receiving PSLF.

Notably, about one-third of all requests have been denied to this date, suggesting that quite a few students will get an unpleasant surprise when they go apply for PSLF in the next few years. But at least 430,000 students look to be on track for PSLF at this point—a number that is likely a significant understatement of the number of applications that the federal government will receive.

1 The Direct Loan program represents about 90% of all loans held by the federal government. The other 10% are in the older Federal Family Education Loan (FFEL) program, which has not disbursed new loans in years but has about one-third of its loan dollars in income-based plans. I excluded FFEL here because repayment plan data are only available for 2016.

3 thoughts on “Income-Driven Repayment Plans Continue to Grow”

Comments are closed.