NOTE: This post was updated April 3 to reflect the Department of Education’s latest release of data on heightened cash monitoring.

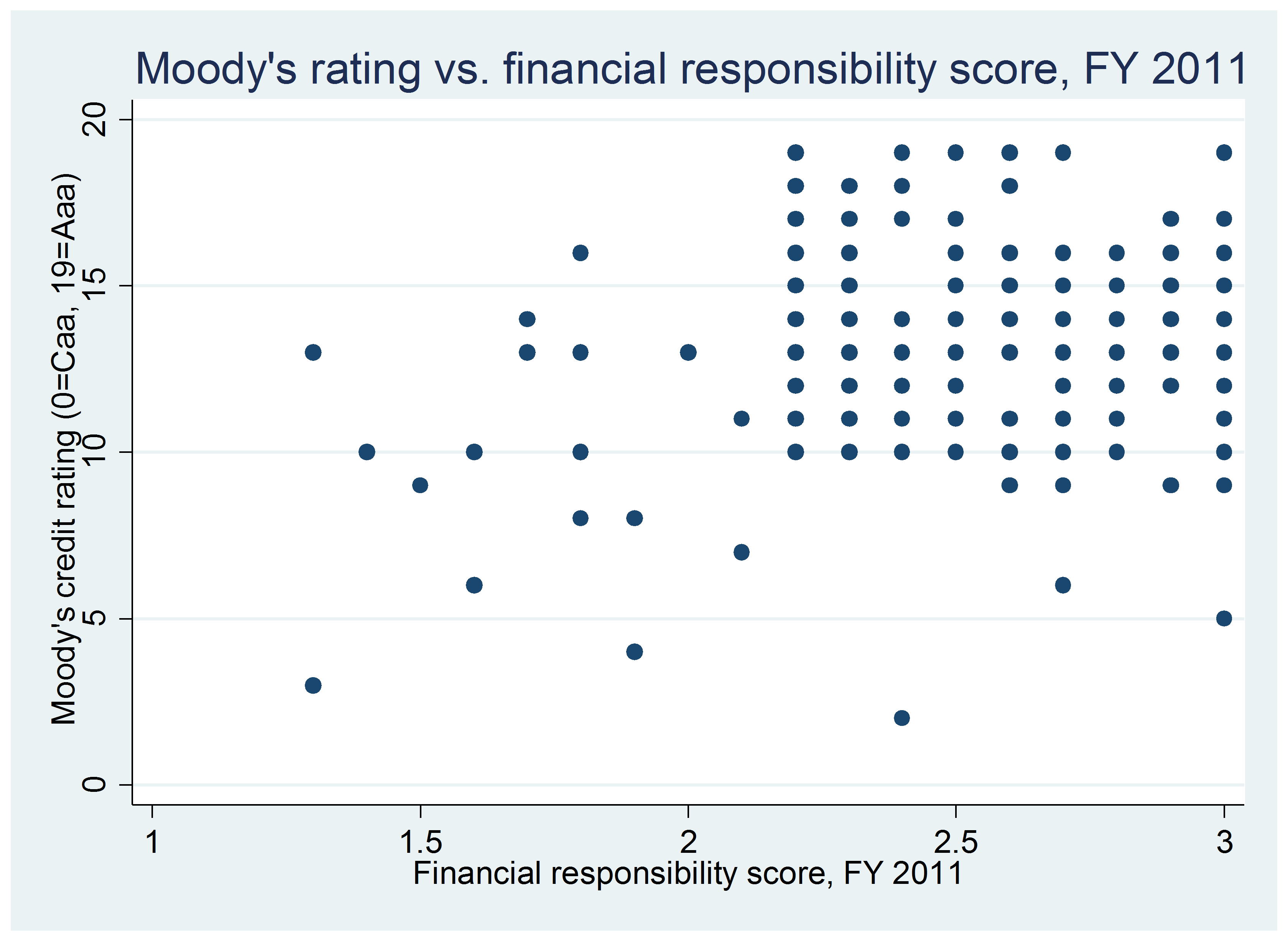

In my previous post, I wrote about the U.S. Department of Education’s release of a list of 544 colleges subject to heightened cash monitoring standards due to various academic, financial, and administrative concerns. I constructed a dataset of the 512 U.S. colleges known to be facing heightened cash monitoring (HCM) along with two other key accountability measures: the percentage of students who default on loans within three years (cohort default rates) and an additional measure of private colleges’ financial strength (financial responsibility scores). In this post, I examine the reasons why colleges face heightened cash monitoring, as well as whether HCM correlates with the other accountability metrics.

The table below shows the number of colleges facing HCM-1 (shorter delays in ED’s disbursement of student financial aid dollars, although colleges not facing HCM have no delays) and HCM-2 (longer delays) by type of institution (public, private nonprofit, and for-profit).

| Table 1: HCM status by institutional type. | ||

| Sector | HCM-1 | HCM-2 |

| Public | 68 | 6 |

| Private nonprofit | 97 | 18 |

| Private for-profit | 284 | 39 |

| Total | 449 | 63 |

While only six of 74 public colleges are facing HCM-2, more than one in ten private nonprofit (18 of 115) and for-profit colleges (39 of 323) are facing this higher standard of oversight. The next table shows the various reasons listed for why colleges are facing HCM.

| Table 2: HCM status by reason for additional oversight. | ||

| Reason | HCM-1 | HCM-2 |

| Low financial responsibility score | 320 | 4 |

| Financial statements late | 66 | 9 |

| Program review | 1 | 21 |

| Administrative capability | 22 | 7 |

| Accreditation concerns | 1 | 12 |

| Other | 39 | 10 |

More than two-thirds (320) of the 449 colleges facing HCM-1 are included due to low financial responsibility scores (below a 1.5 on a scale ranging from -1 to 3), but only four colleges are facing HCM-2 for that reason. The next most common reason, affecting 75 colleges, is a delayed submission of required financial statements or audits. This affected 43 public colleges in Minnesota, which are a majority of the public colleges subject to HCM. Program review concerns were a main factor for HCM-2, with 21 colleges in this category (including many newly released institutions) facing HCM-2. Other serious concerns included administrative capability (22 in HCM-1 and 7 in HCM-2), accreditation (2 in HCM-1 and 12 in HCM-2), and a range of other factors (39 in HCM-1 and 10 in HCM-2).

The next table includes three of the most common or serious reasons for facing HCM (low financial responsibility scores, administrative capacity concerns, and accreditation issues) and examines their median financial responsibility scores and cohort default rates.

| Table 3: Median outcome values on other accountability metrics. | ||

| Reason for inclusion in HCM | Financial responsibility score | Cohort default rate |

| Low financial responsibility score | 1.2 | 12.1% |

| Administrative capability | 1.6 | 20.3% |

| Accreditation issues | 2.0 | 2.8% |

Not surprisingly, the typical college subject to HCM for a low financial responsibility score had a financial responsibility score of 1.2 in Fiscal Year 2012, which would require additional federal oversight. Although the median cohort default rate was 12.1%, which is slightly lower than the national default rate of 13.7%, some of these colleges do not participate in the federal student loan program and are thus counted as zeroes. The median college with administrative capability concerns barely passed the financial responsibility test (with a score of 1.6), while 20.3% of students defaulted. Colleges with accreditation issues (either academic or financial) had higher financial responsibility scores (2.0) and lower cohort default rates (2.8%).

What does this release of heightened cash monitoring data tell us? Since most colleges are on the list for known concerns (low financial responsibility scores or accreditation issues) or rather silly errors (forgetting to submit financial statements on time), the value is fairly limited. But there is still some value, particularly in the administrative capability category. These colleges deserve additional scrutiny, and the release of this list will do just that.