The Trump administration released its first full budget proposal for Fiscal Year 2018 today, and it is safe to say that it represents a sharp break from the Obama administration’s budget proposals. The proposed discretionary budget for the Department of Education is about $69 billion, $10 billion less than the Fiscal Year 2017 budget. Below, I offer brief comments on three of the key higher education proposals within the budget, as well as my take on whether the proposals are likely to be enacted in some form by a Republican-controlled Congress that seems fairly skeptical of the Trump administration’s higher education policy ideas.

Public Service Loan Forgiveness would no longer be available for new borrowers. Public Service Loan Forgiveness (PSLF) was first made available in 2007 in an effort to encourage individuals to work in lower-paying nonprofit or government jobs. This plan allows students enrolled in income-driven repayment plans who annually certified their income and employment status to have any remaining balances forgiven after ten years of payments of 10% of discretionary income. However, the plan has been criticized due to its likely high price tag to taxpayers and because it provides far larger subsidies to graduate students than undergraduate students.

The Trump administration’s budget proposal would end PSLF for new borrowers as of July 1, 2018—and require all people currently on PSLF to maintain continuous enrollment in the program to remain eligible. This is likely to be a difficult hurdle for many people to clear, as a large number of students have been tripped up by annual recertification in the past. I’m glad to see that the Trump administration didn’t completely end PSLF for current students (as people reasonably relied on the program to make important life choices), but otherwise saving PSLF in the current form isn’t at the top of my priority list because of how most of the subsidy goes to reasonably well-off people with graduate degrees instead of low-paid individuals with a bachelor’s degree in early childhood education.

Prognosis of happening: Low to medium. This will generate howls of outrage in The New York Times and The Washington Post from groups such as the American Bar Association and the National Education Association, but there is a reasonable argument for at least curtailing the amount of money that can be forgiven under PSLF. A full-fledged ending of the program may not happen, but some changes are quite possible as quite a few members of Congress are upset with rising costs of loan forgiveness programs.

Subsidized loans for undergraduates would be eliminated, and income-driven loan repayment periods would change. Undergraduate students can qualify for between $3,500 and $5,500 per year in subsidized student loans (meaning interest is not charged while they are in school), with the remainder of their federal loans being unsubsidized (with interest accumulating immediately). The Trump administration would end subsidized loans, with the likely rationale that the interest subsidy is not an efficient use of resources (something that is hard to empirically confirm or deny, but is quite plausible).

The federal government currently offers students a menu of income-driven loan repayment options, and the Trump administration proposed to simplify these into one option. Undergraduates would pay up to 12.5% of the income over 15 years (from 10% over 20 years for the most popular current plan), while grad students would pay up to 12.5% for 30 years. Undergraduate students probably benefit from this change, while graduate students decidedly do not. This plan hits master’s degree programs hard, as any graduate debt would either trigger a 30-year repayment period for a potentially small amount of additional debt or push people back into a standard (non-income-driven) plan.

Prognosis of happening: Medium. There has been a great deal of support for streamlining income-driven repayment plans, but the much less-generous terms for graduate students (along with ending PSLF) would significantly affect graduate student enrollment. This will mobilize the higher education community against the proposal, particularly as many four-year colleges are seeking to grow graduate enrollment as a new revenue source. But potentially moving to a 20-year repayment period for graduate students or tying repayment length to loan debt are more politically feasible. The elimination of subsidized loans for undergraduates hits low-income students, but a more generous income-driven repayment program mainly offsets that and makes that change more realistic.

Federal work-study funds would be cut in half and the Supplemental Educational Opportunity Grant would be eliminated. The federal government provides funds for these two programs to individual colleges instead of directly to students, and colleges are required to provide matching funds. The SEOG is an additional grant available to needy undergraduates at participating colleges, while federal work-study funds can go to undergraduate or graduate students with financial need. Together, these programs provide about $1.7 billion of funding each year, with funds disproportionately going to students at selective and expensive colleges due to an antiquated funding formula. Rather than fixing the formula, the Trump administration proposed to get rid of SEOG (as being duplicative of Pell) and halve work-study funding.

Prognosis of happening: Slim to none. Because funds disproportionately go to wealthier colleges (and go to colleges instead of students), the lobbying backlash against cutting these programs will be intense. (There is also research evidence showing that work-study funds do benefit students, which is important to note as well.) Congressional Republicans are likely to give up on changing these two programs in an effort to focus on higher-stakes changes to student loan programs.

In summary, the Trump administration is proposing some substantial changes to how students and colleges are funded. But don’t necessarily expect these changes to be implemented as proposed, even if there are plenty of concerns among conservatives about the price tag and inefficient targeting of current federal financial aid programs. It will be crucial to see the budget bill that will go up for a vote in the House of Representatives, as that is more likely to be passed into law than the president’s proposed budget.

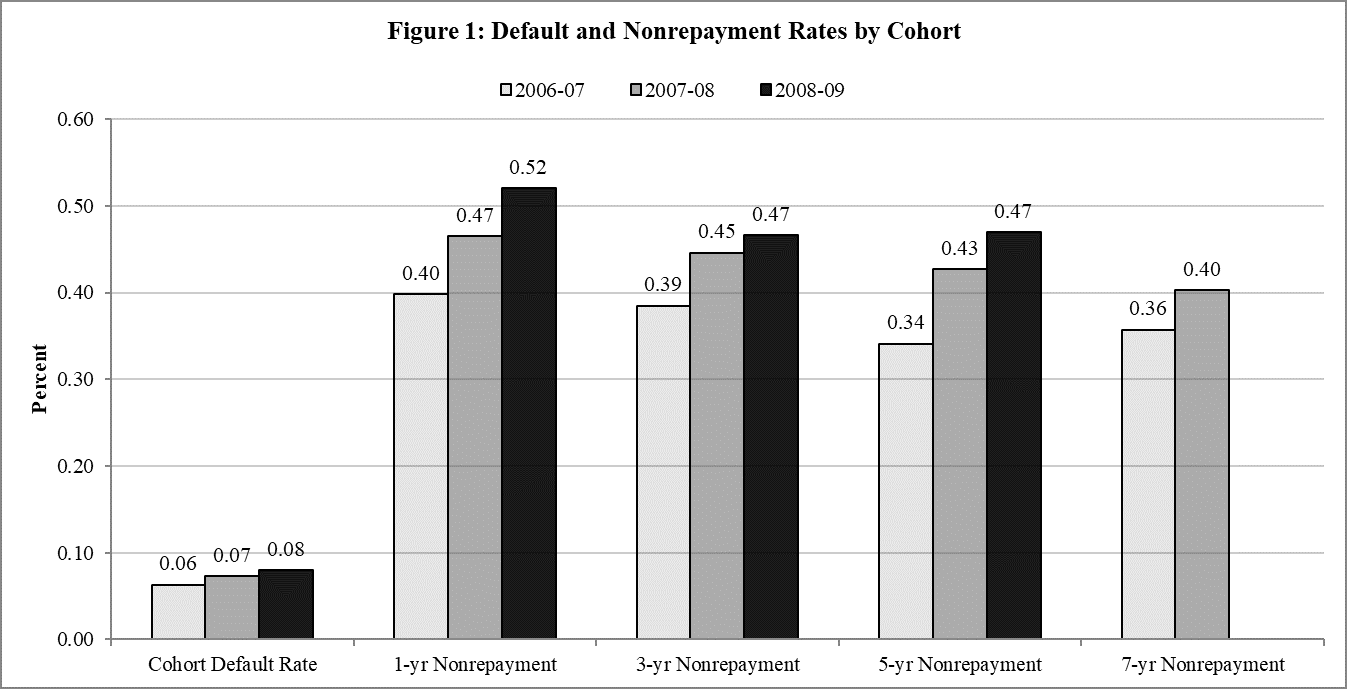

An advantage of the PowerStats tool is that it allows users to run regressions via NCES’s remote server. This allows interested people to analyze the relationship between long-term default rates and attending a for-profit college after controlling for other characteristics. However, PowerStats is overwhelmed by requests by my fellow higher education data nerds at this point, so I gave up on trying to run the regression after several hours of waiting. But if someone wants to run some regressions using the new loan repayment data in the BPS once the server calms down, I’m happy to feature their work on my blog!

An advantage of the PowerStats tool is that it allows users to run regressions via NCES’s remote server. This allows interested people to analyze the relationship between long-term default rates and attending a for-profit college after controlling for other characteristics. However, PowerStats is overwhelmed by requests by my fellow higher education data nerds at this point, so I gave up on trying to run the regression after several hours of waiting. But if someone wants to run some regressions using the new loan repayment data in the BPS once the server calms down, I’m happy to feature their work on my blog!