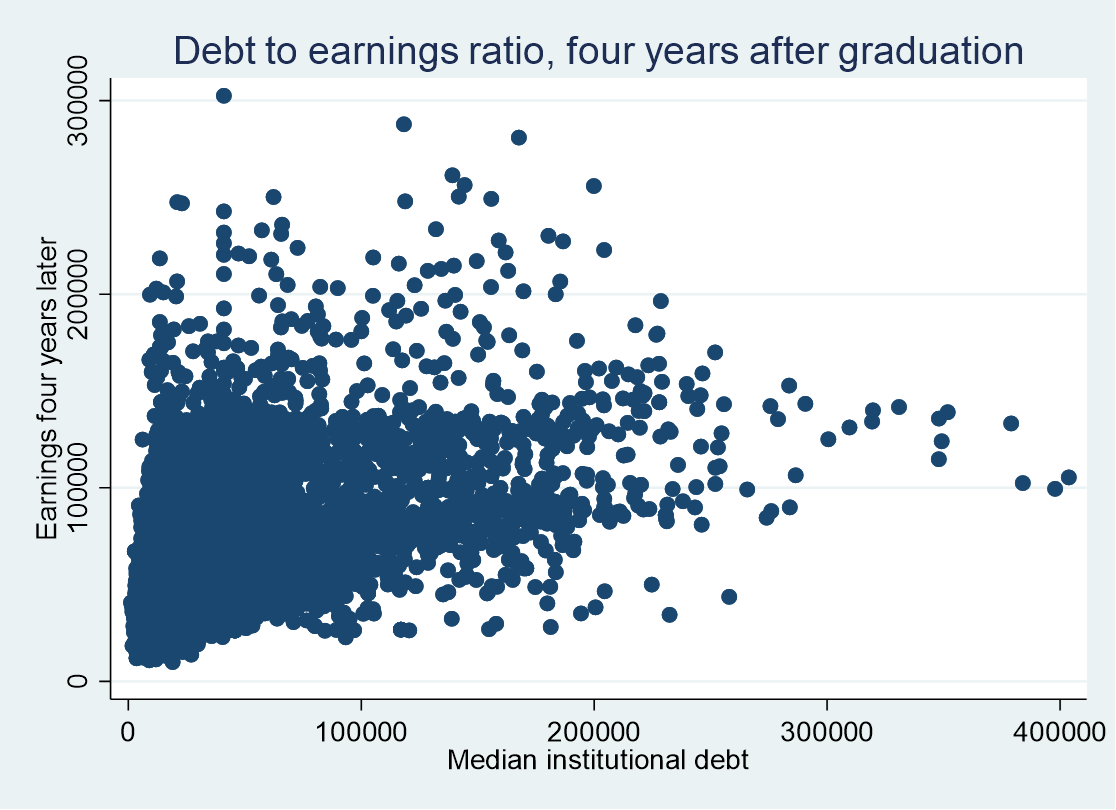

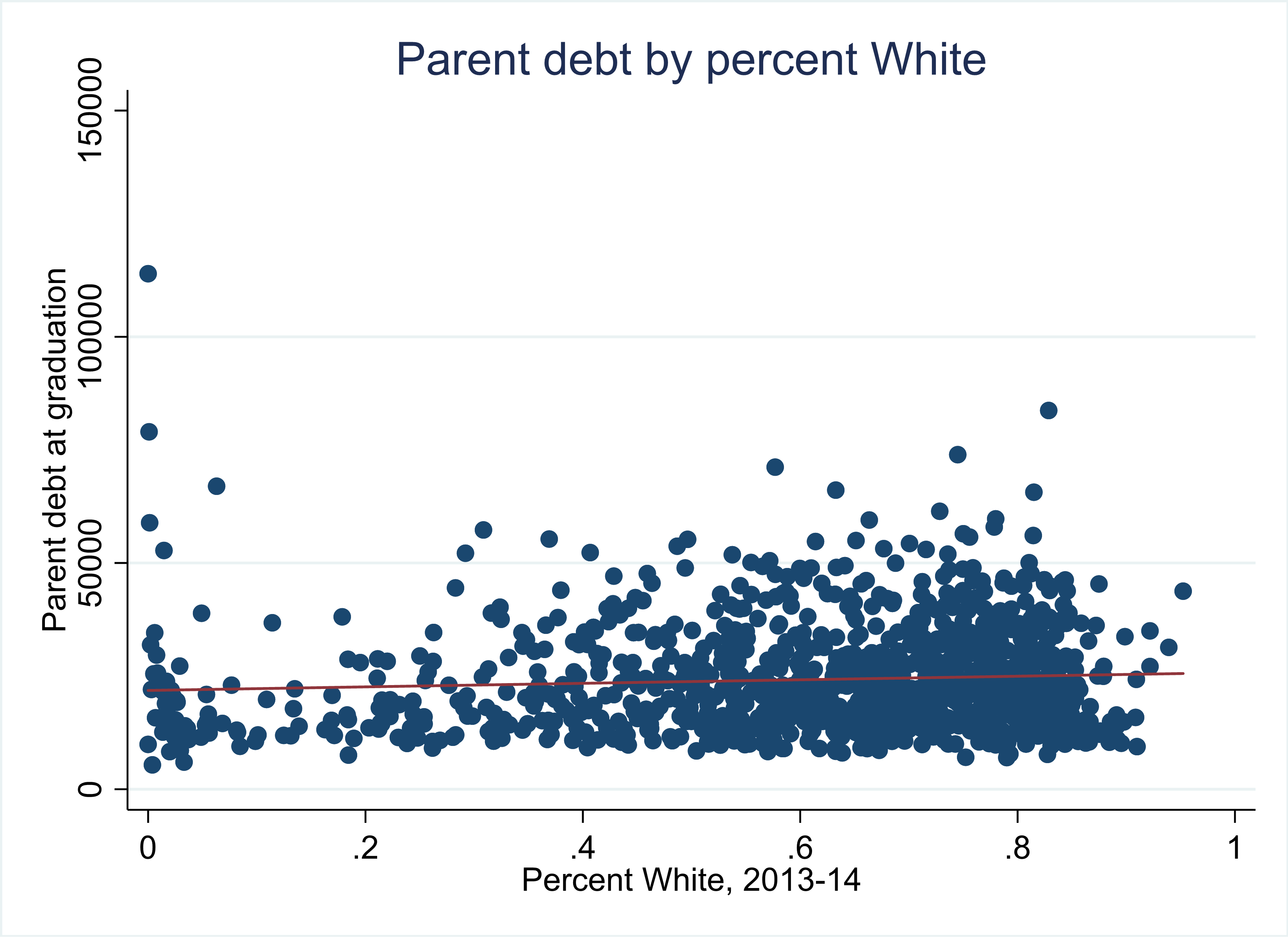

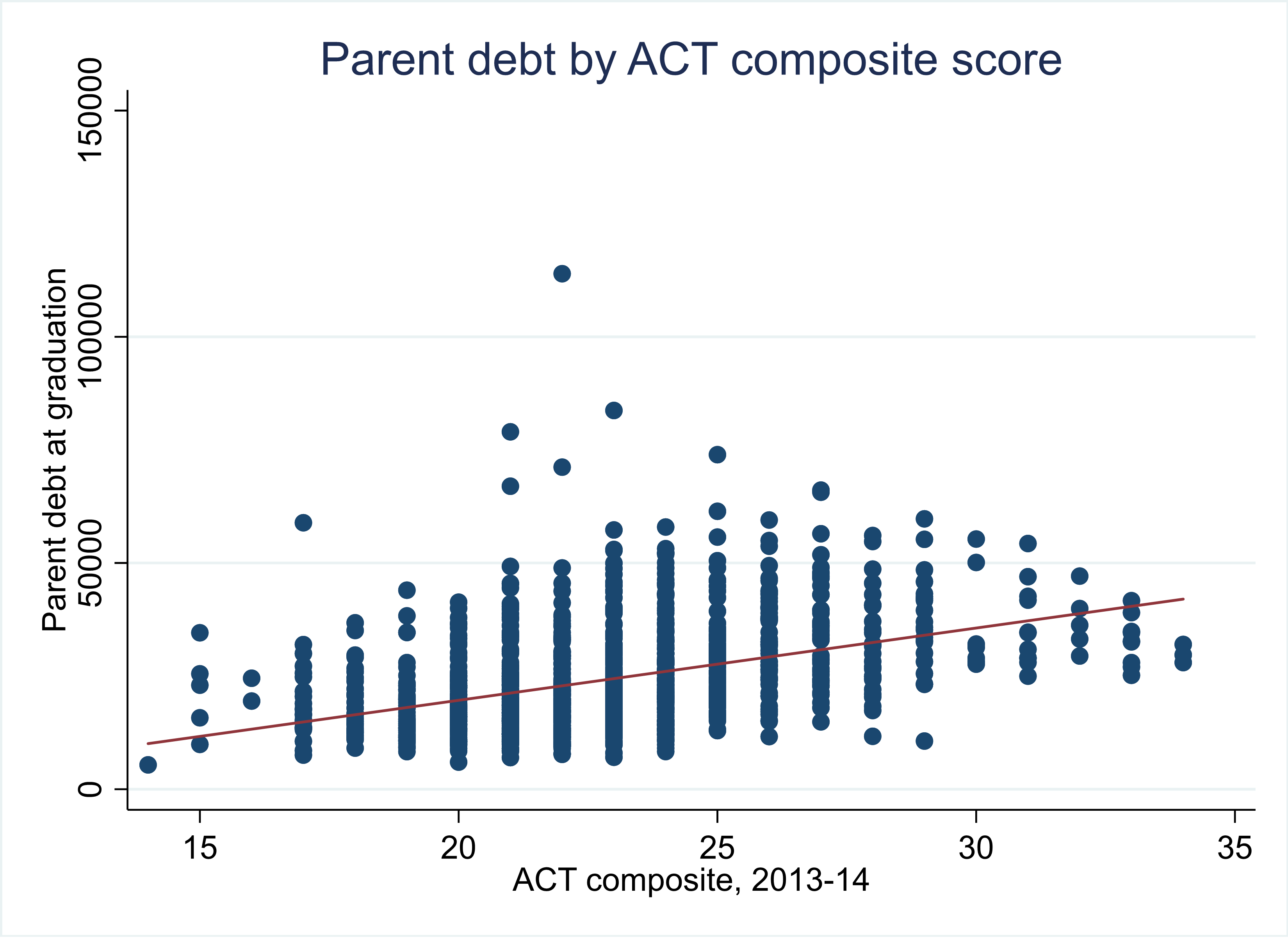

The Department of Education’s updated College Scorecard dataset contains two new features at the program level. (I looked at the new institution-level data in my previous post.) The first feature is information on median Parent PLUS loan debt and the number of students whose parents take on debt. The second is earnings two years after graduation, which added onto last year’s one-year data.

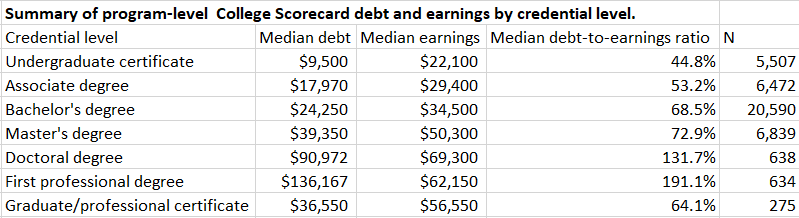

In this post, I constructed a dataset of students who graduated in the 2014-15 and 2015-16 academic years combined with one-year earnings from calendar years 2016 and 2017 and two-year earnings from calendar years 2017 and 2018. (A note to analysts: the most recent data file shows debt for the 2016-17 and 2017-18 graduating cohorts, one-year earnings from the 2015-16 and 2016-17 cohorts, and two-year earnings from the 2014-15 and 2015-16 cohorts. This will result in some funky numbers, so download the big dataset instead and do your own merging.) I then pulled data for fields of study that had data from 50 or more programs at each credential level.

You can download my summary dataset here, and some key findings are below.

Undergraduate certificate

Both earnings and debt burdens are typically fairly low, and two-year earnings were always higher than one-year earnings (which was true across all programs and credential levels). The median cosmetology graduate had (reported) earnings of just $17,821 two years after graduation, but median student debt was $12,851, only about 14% of student borrowers had their parents take on Parent PLUS loans, and median PLUS debt was just $7,397. Vehicle maintenance and repair had the second-highest two-year earnings ($33,632, just behind nursing at $34,108), but about 34% of borrowers had Parent PLUS loans of nearly $15,000.

Associate degree

Parent PLUS loans were relatively uncommon at this level, with the exception of culinary arts (about 20% of students had parents with PLUS debt). Registered nurses earned $57,247 per year, far higher than any other field. Liberal arts/general studies graduates had modest earnings ($26,159), but their student debt burdens of $13,452 were at least $10,000 below all other fields of study.

Bachelor’s degree

Earnings two years after graduation ranged from $25,243 in fine arts to $66,218 in mechanical engineering. A large number of majors clustered between $30,000 and $35,000 in earnings, while student debt was typically between $25,000 and $31,000. Fields dominated by adults, such as health/medical administration, had much higher student debt burdens due to their ability to access higher independent loan limits. PLUS loan amounts typically ranged between $20,000 and $30,000, but human resources ($13,637), liberal arts (16,450), design ($40,231) and film ($46,006) stood out as outliers. Film was also a concern in that about 41% of student borrowers also had Parent PLUS loans. This compares to fields like business and nursing, where 10%-15% of students had their parents take on loans.

Master’s degree

The variation in debt (from that institution only) and earnings was much larger for master’s degrees. Two-year earnings ranged from $27,941 in music to $102,895 in earnings, and debt ranged from $27,492 in curriculum and instruction to $95,823 in allied health. Only six programs had debt burdens larger than second-year earnings, led by mental health services at 1.43. Surprisingly, theology graduates (at $44,485) earned nearly as much as criminal justice graduates (at $46,269).

Doctoral degrees

Based on these data alone, going to medical school looks like a terrible life choice as two-year earnings were $58,056 compared to debt of $167,169. However, most new medical doctors do a residency of three years or so before launching into a well-paid career. Pharmacy and nursing graduates see six-figure salaries from the start and have less debt. And I have to give a shout-out to educational administration programs. The overall numbers are solid (earnings of $79,713 compared to debt of $68,877). Graduates of the department that I chair at Seton Hall earned $111,435 with debt of $62,841. Time to hit people up for donations???