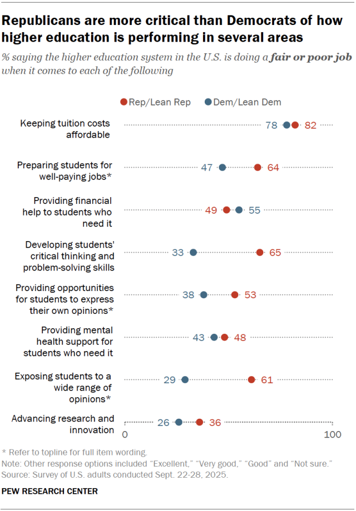

Higher education is facing a crisis of confidence among the general public, and much of that is driven by concerns regarding affordability. For example, about 80 percent of Democrats and Republicans alike think that colleges do not sufficiently prioritize affordability.

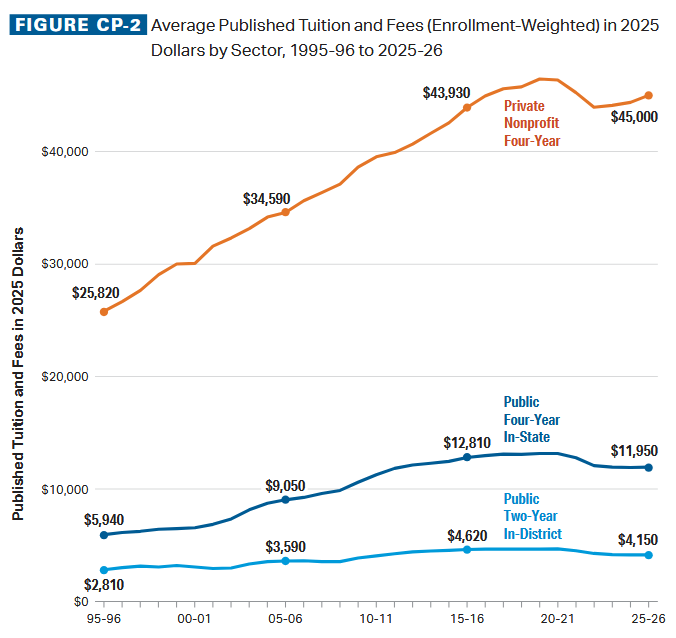

But while college is still expensive, the narrative that colleges and universities are increasing their tuition willy-nilly has not been true for a decade. See this chart from the College Board’s helpful Trends in College Pricing report, which has data through the 2025-26 academic year—two years ahead of U.S. Department of Education data. Tuition increases have been at or below inflation for the last decade, breaking a decadeslong trend of increases well above the rate of inflation.

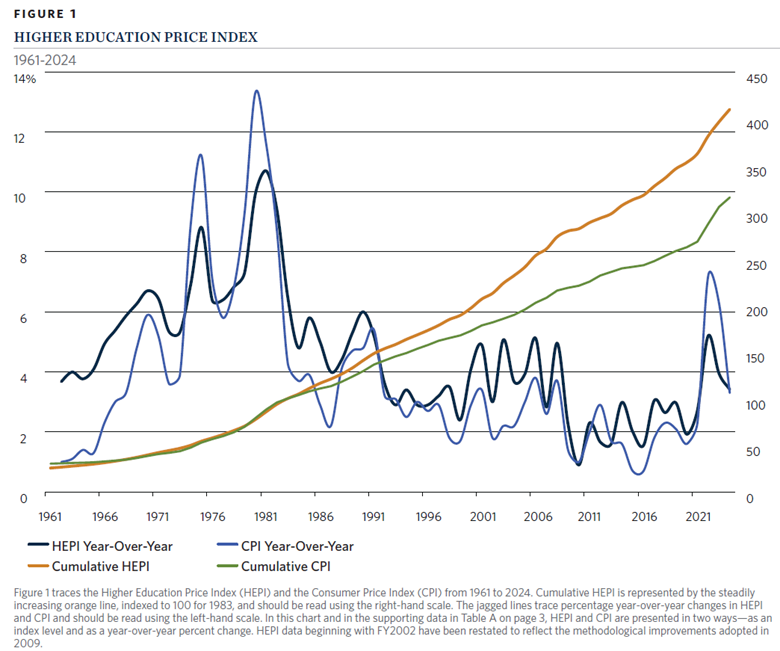

This is why I was disappointed to see a recent NPR piece that focused on how college costs (which should be prices—grrrr) have doubled in inflation-adjusted dollars in the last three decades. (The headline of doubling over 20 years is inaccurate, but it is right in the main part of the piece at 30 years.) Yes, listed tuition and fees doubled between 1995 and 2015, but they have not budged in the last decade. And if grant aid is taken into account, much of higher education is close to pre-Great Recession affordability. That is in spite of operating costs (as proxied by the Higher Education Price Index) rising faster than inflation over much of the period, driven by benefits and maintenance costs.

This more nuanced narrative (affordability is still a concern, but the situation has actually improved in public higher education) is important to communicate to the general public. The NPR piece was spot-on in 2015, but less so in 2025.

With all that being said, colleges are under more pressure to generate revenue than at any point in recent years. State funding has been an unsung hero for the last decade, and that is likely to take a hit as budgets get tight. With all of the pressures coming out of Washington, institutions are likely to turn to larger tuition increases if at all possible. Public institutions are frequently constrained by state-level tuition controls, which are present in about 30 states. But other public and private institutions may try to get more revenue out of tuition, breaking a promising trend that few people outside of higher education even knew was in progress.

For the first time in the lifetimes of many Americans, inflation has become a legitimate concern. In the last year, the Consumer Price Index increased at a 6.2 percent clip—a rate not seen this century.

Trends in inflation over the last two decades (BLS graphic)

The higher education industry is far from immune from the effects of an inflationary cycle that was largely unexpected even a few months ago. Colleges have been strugglingto address supply chain issues and a shortage of staff members willing to work in person at pre-pandemic wage rates. Colleges have responded by reducing services, increasing wages in some cases, and even trying to get faculty members to work in dining halls. In my position as a faculty member and department head, I am still waiting for my permanent laptop computer setup to arrive and have seen the challenges in trying to hire employees within existing salary bands.

But what really caught my attention was Virginia Tech’s move to increase meal plan charges by about $200 between the fall and spring semesters. Midyear adjustments in student charges are highly unusual and typically only happen if a state withholds previously promised funding during a recession. But the university is required by state law to have auxiliary enterprises operate with balanced budgets, so the sudden increase in costs had to be passed on to students.

At this point, it seems like inflationary pressures are here to stay for at least the next several months. This will put continued pressure on colleges to increase their salaries to keep up with a hot economy and rising consumer prices. While faculty tend to have less power in the labor market due to lots of qualified people looking to teach in many disciplines, many staff members are in a great position to command raises of between five and ten percent as colleges look to retain talent.

This is also the time of year during which many colleges start to develop their proposed rates for tuition, fees, and room and board for the next (2022-23) academic year. With the costs of running a college likely to rise by at least five percent this year, the logical step for colleges would be to raise student charges by the same amount. This would be a rate largely unseen since the Great Recession—when student debt was less of a public policy concern and there was less vocal skepticism of higher education. But if colleges try to keep tuition increases more modest, they are losing money. And that is a challenge after the pandemic severely affected the finances of many institutions.

So expect a fair amount of sticker shock this spring when tuition, housing, and dining charges for next year get posted. There are likely to be three types of exceptions to this trend:

Public colleges in states that limit tuition increases by state law or governing board policy. They’re stuck with what they can get.

Extremely wealthy colleges that can afford to limit increases if that will help them increase diversity and/or move up in the rankings.

Cash-strapped colleges that are desperately seeking to recruit and retain students. They will decide that holding the line on student charges is the best of a lousy set of options.

Greetings from beautiful eastern Tennessee! Since my last post, I have accepted a position as professor and head of the Department of Educational Leadership and Policy Studies at the University of Tennessee, Knoxville. It is an incredible professional opportunity for me, and the Knoxville area is a wonderful place to raise a family. I start on August 1, so the last month has been a combination of moving, taking some time off, and getting data in order to keep making progress on research.

Speaking of getting new data in order, the U.S. Department of Education’s newest iteration of Integrated Postsecondary Education Data System (IPEDS) data came out with a fresh year of data on tuition and fee charges, enrollment, and completions. In this post, I am using the new data on tuition and fees in the 2020-21 academic year to look at how colleges changed their listed prices during the pandemic.

I limited my analysis to 3,356 colleges and universities that met three criteria. First, they had IPEDS data on in-district or in-state tuition and fees in both the 2019-20 and 2020-21 academic years. Second, they reported data for the typical program of study (academic year reporters) instead of separately for large programs (program reporters). This excluded most certificate-dominant institutions. Third, I kept colleges with Carnegie classifications in 2018 and excluded tribal colleges due to their unique governance structures. I then classified public institutions into two-year and four-year colleges based on Carnegie classifications to properly classify associate-dominant institutions as two-year colleges.

Now on to the analysis. There was a lot of coverage of colleges cutting tuition and/or fees for 2020-21 on account of the pandemic, but now analysts can see how prevalent this actually was. The majority of public and for-profit colleges either froze or decreased tuition in 2020-21, but two-thirds of private nonprofit colleges increased their list prices. This does not mean that private colleges actually increased tuition revenue due to the possibility of increased financial aid, and this answer will not be known in publicly available data until early 2023. Public colleges and universities were somewhat more likely to reduce fees than tuition, while for-profit colleges were less likely to do so.

The rightmost column of the first table below combines tuition and fees and provides a more comprehensive picture of student charges. Although a majority of public universities froze tuition and fees, combined tuition and fees still increased at 56% of institutions. This suggests that colleges that froze tuition increased fees and colleges that froze fees increased tuition. Colleges found a way to get the money that they needed. Fifty-three percent of community colleges increased tuition and fees, while 71% of private nonprofit colleges did so compared to just 42% of for-profit colleges.

Changes in tuition and fees, 2019-20 to 2020-21.

Tuition

Fees

Tuition and fees

Four-year public

Increase

35.6%

35.8%

56.1%

No change

61.2%

55.5%

30.7%

Decrease

3.2%

8.6%

13.1%

Two-year public

Increase

41.0%

45.1%

53.4%

No change

55.3%

40.0%

39.9%

Decrease

3.8%

14.9%

6.6%

Private nonprofit

Increase

66.9%

38.6%

71.2%

No change

28.2%

54.0%

21.3%

Decrease

4.9%

7.4%

7.5%

For-profit

Increase

34.7%

25.3%

42.3%

No change

49.6%

66.8%

41.5%

Decrease

15.7%

7.8%

16.2%

Source: Robert Kelchen’s analysis of IPEDS data.

The next obvious question is whether the 2020-21 trends differed from past years. I pulled IPEDS data going back to 2015 to look at trends in tuition and fees over the past five years. The share of tuition freezes increased in every sector of higher education, with the increase being most pronounced among public universities (9.5% in 2019-20 to 30.7% in 2020-21). Other sectors had smaller increases, although around one-third of community colleges and for-profit institutions had no changes in tuition and fees in prior years. The only sector with a large increase in tuition and fee cuts was public universities, with a jump from 5.1% to 13.1% between 2019-20 and 2020-21.

Changes in tuition and fees over time.

4-year public

2-year public

Private nonprofit

For-profit

2020-21

No change

30.7%

39.9%

21.3%

41.5%

Decrease

13.1%

6.6%

7.5%

16.2%

2019-20

No change

9.5%

31.7%

13.7%

34.0%

Decrease

5.1%

6.9%

4.7%

12.0%

2018-19

No change

10.5%

27.2%

14.6%

38.0%

Decrease

6.0%

6.5%

5.2%

22.4%

2017-18

No change

7.4%

27.2%

12.4%

34.8%

Decrease

3.2%

5.9%

3.6%

25.0%

2016-17

No change

13.8%

24.5%

12.4%

28.7%

Decrease

4.4%

8.0%

3.8%

16.0%

2015-16

No change

8.7%

29.3%

10.8%

33.5%

Decrease

5.2%

7.3%

4.3%

18.2%

Source: Robert Kelchen’s analysis of IPEDS data.

As the pandemic enters a new stage, the higher education community continues to get more information on the broader effects on the 2020-21 academic year. It will take a few years to get a complete picture of what happened in the sector, but each data release provides additional insights for researchers and policymakers.

I have long been interested in studying how colleges use their revenue, so I began sketching out a paper looking at whether public universities appeared to use additional revenue from out-of-state students to improve affordability for in-state students. Since I am particularly interested in prices faced by students from lower-income families, I was also concerned that any potential increase in amenities driven by out-of-state students could actually make college less affordable for in-state students.

I started working on this project back in the spring of 2015 and enjoyed two and a half conference rejections (one paper submission was rejected into a poster presentation), two journal rejections, and a grant application rejection during the first two years. But after getting helpful feedback from the journal reviewers (unfortunately, most conference reviewers provide little feedback and most grant applications are rejected with no feedback), I made improvements and finally got the paper accepted for publication.

The resulting article, just published in Teachers College Record (and is available for free for a limited time upon signing up as a visitor), includes the following research questions:

(1) Do the listed cost of attendance and components such as tuition and fees and housing expenses for in-state students change when nonresident enrollment increases?

(2) Does the net price of attendance (both overall and by family income bracket) for in-state students change when nonresident enrollment increases?

(3) Do the above relationships differ by institutional selectivity?

After years of working on this paper and multiple iterations, I am pleased to report…null findings. (Seriously, though, I am glad that higher education journals seem to be willing to publish null findings, as long as the estimates are precisely located around zero without huge confidence intervals.) These findings suggest two things about the relationship between nonresident enrollment and prices faced by in-state students. First, it does not look like nonresident tuition revenue is being used to bring down in-state tuition prices. Second, it also does not appear that in-state students are paying more for room and board after more out-of-state students enroll, suggesting that any amenities demanded by wealthier out-of-state students may be modest in nature.

I am always happy to take any questions on the article or to share a copy if there are issues accessing it. I am also happy to chat about the process of getting research published in academic journals, since that is often a long and winding road!