Net price calculators are designed to give students and their families a clear idea of how much college will cost them each year after taking available financial aid into account. All colleges have to post a net price calculator under the Higher Education Opportunity Act of 2008, but these calculators take a range of different form. The Department of Education has proposed a standardized “shopping sheet” which has been adopted by some colleges, but there is still a wide amount of variation in net price calculators across institutions. This is shown in a 2012 report by The Institute for College Access and Success, using 50 randomly selected colleges across the country.

In this blog post, I examine net price calculators from six University of Wisconsin System institutions for the 2013-14 academic year. Although these colleges might be expected to have similar net price calculators and cost assumptions, this is far from the case as shown in the below screenshots. In all cases, I used the same student conditions—an in-state, dependent, zero-EFC student.

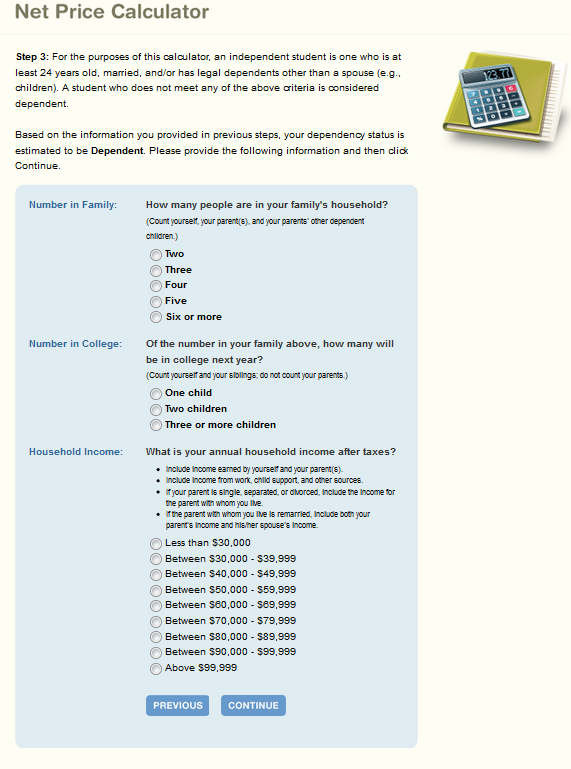

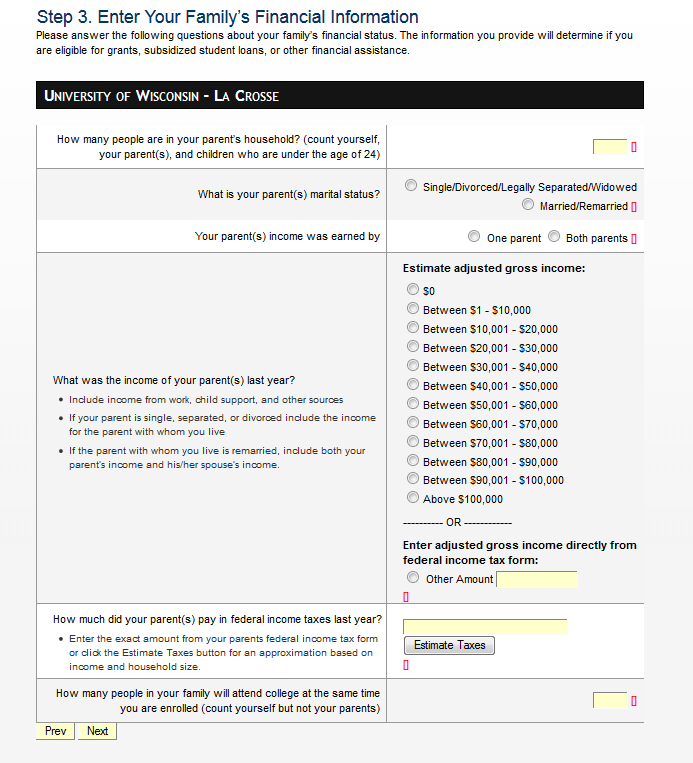

Two of the six colleges selected (the University of Wisconsin Colleges and UW-La Crosse) require students to enter several screens of financial and personal information in order to get an estimate of their financial aid package. While that can be useful for some students, there should be an option to directly enter the EFC for students who have filed the FAFSA or are automatically eligible for a zero EFC. For the purposes of this post, I stopped there with those campuses—as some students may decide to do.

(UW Colleges and UW-La Crosse, respectively)

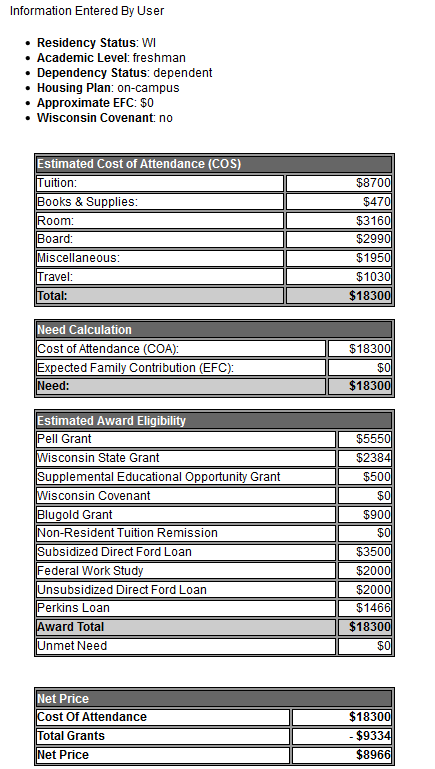

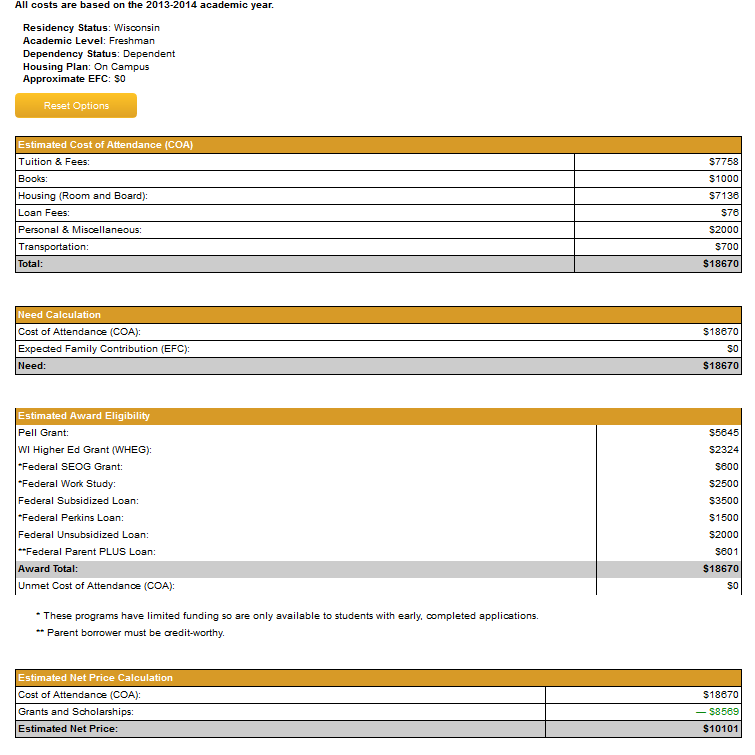

UW-Milwaukee deserves special commendation for clearly listing the net price before mentioning loans and work-study. Additionally, they do not list out each grant a student could expect to receive, simplifying the information display (although this does have its tradeoffs).

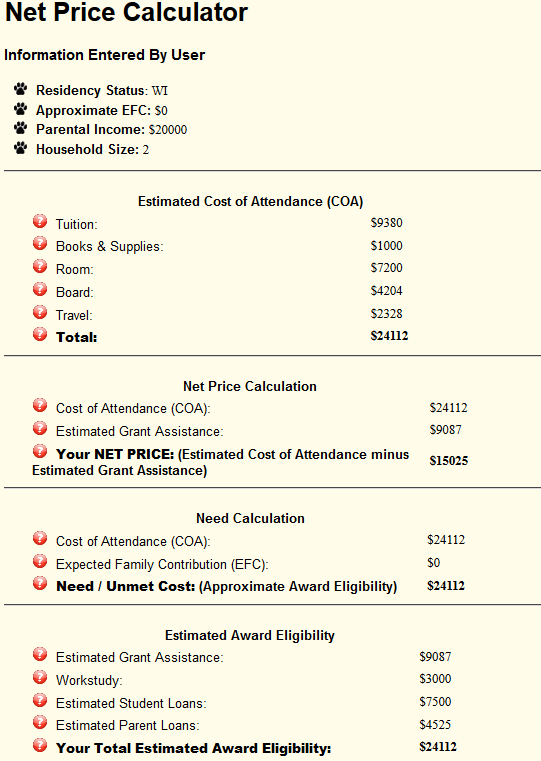

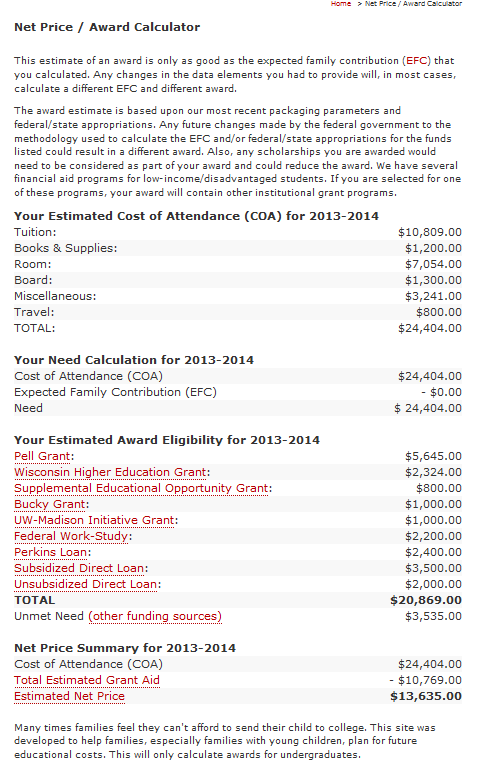

The other three schools examined (Eau Claire, Madison, and Oshkosh) list out each type of financial aid and present an unmet need figure (which can be zero) before reporting the estimated net price of attendance. Students may read these calculators and think that no borrowing is necessary in order to attend college, while this is not the case. The net price should be listed first, since this tool is a net price calculator.

(UW-Eau Claire, UW-Madison, and UW-Oshkosh, respectively)

The net price calculators also differ in their terminologies for different types of financial aid. For example, UW-Eau Claire calls the Wisconsin Higher Education Grant the “Wisconsin State Grant,” which appears nowhere else in the information students receive. The miscellaneous and travel budgets vary by more than $1000 across the four campuses with net price calculators, highlighting the subjective nature of these categories. However, they are very important to students because they cannot receive more in financial aid than their total cost of attendance. If colleges want to report a low net price, they have incentives to report low living allowances.

I was surprised to see the amount of variation in net price calculators across UW System institutions. I hope that financial aid officers and data managers from these campuses can continue to work together to refine best practices and present a more unified net price calculator.