Yesterday, I unveiled my fifth annual list of the top ten events in American higher education in 2017. Now it’s time for the annual list of the “not top ten” events—which are a mix of puzzling decisions and epic fails that leave most of us wondering what people were thinking. Enjoy the list—and send along any feedback that you have!

(10) Sorority rush consultants are apparently a real thing. Higher education is no stranger to consultants—they are used to help with presidential searches, deal with tough budget issues, and conduct research for colleges and universities. The college admissions process for higher-income families is also full of consultants, including private admissions counselors, test prep agencies, and tutors. But I had never thought about the need for “sorority rush consultants” before reading this fascinating piece in Town and Country magazine (which prominently features a “society” section). There seems to be no limit to how much money wealthy families are willing to pay for their children to have every possible advantage—or alternatively, it’s quite easy to part people from their money when something college-related is at stake.

(9) 71% of college presidents oppose giving the public basic information about student outcomes via the College Scorecard. Inside Higher Ed’s annual survey of college presidents found deep disdain for the College Scorecard—the first time that college-level outcomes such as student loan repayment rates, debt burdens, and earnings were available to the general public. Opposition was strongest among private college presidents (who are the only sector of higher education to oppose a federal student-level dataset), but a majority of public college presidents also opposed the Scorecard. To me, federal financial aid access in exchange for basic outcomes data seems like a reasonable trade-off, but there is probably a reason why I’m not a college president.

(8) Rutgers chancellor says rankings are the university’s biggest problem. As someone who compiles a set of college rankings each year, it may be strange for me to argue with the chancellor of Rutgers University’s flagship New Brunswick campus for saying the following:

“The No. 1 problem is how does Rutgers reflect itself accurately in all the national rankings?”

I still can’t believe that Debasish Dutta thinks that rankings are that big of a concern, given issues about affordability, a decline in high school graduates in the Northeast, and a struggling state pension system that Rutgers participates in. But again, there is probably a reason why I’m not a college president.

(7) Two women face 20 years in prison for swindling $24 million in GI Bill benefits from taxpayers through a correspondence course scam. A former associate dean at Caldwell University and an employee of a company called Ed4Mil were able to concoct a scheme worthy of a made-for-TV movie. They would together supposedly enroll veterans in Caldwell’s online classes, but actually place them into correspondence courses that didn’t qualify for GI Bill benefits. Over five years, the two women were able to pocket $24 million in taxpayer funds through this scheme without the university—or its accreditor—finding out about it. But justice finally arrived with the two pleading guilty to wire fraud charges and potentially facing 20 years in prison. Moral of the story: It’s generally a bad idea to try to run fake classes (more on that later).

(6) Monocles everywhere dropped as Harvard suffered the humiliation of having a program fail gainful employment regulations. The initial release of gainful employment data in January showed that 98% of the programs that failed based on debt-to-earnings ratios were at for-profit colleges. But among the nondegree programs at public and private nonprofit colleges that were subject to gainful employment, there were a few surprises. Harvard, Johns Hopkins, and USC all had one program fail, with Harvard choosing to close down its two-year graduate certificate program in theater. Of course, the university could have also used its very limited resources to fully fund students, but they chose to go in a different direction.

(5) College basketball—and the University of Louisville in particular—had a rough year. It’s good for a university’s basketball team to be in the top ten two years in a row—but it’s bad for a university to be in my “not top ten” list in two consecutive years. Yet the University of Louisville claims that dubious honor after the mess regarding its men’s basketball program. Louisville was one of several universities ensnared in a FBI bribery investigation involving shoe companies, which led the university to fire longtime coach Rick Pitino (who got 98% of the proceeds of Louisville’s current apparel contract with Adidas). Pitino then sued the university for $35 million for breach of contract, ensuring this sad saga continues on for a while. On the bright side, at least this scandal doesn’t involve prostitutes.

(4) The Department of Education revealed a monumental coding error in the College Scorecard in the final weekend of the Obama administration. Friday afternoon news dumps have a long and sordid history in the eyes of journalists and the general public, with the goal being to bury bad news when no one else is watching or on duty. In the political world, these news dumps are bipartisan in nature and often expected to happen. On the final Friday of the Obama administration (right before a three-day weekend), a reporter tipped me off to an announcement on the Department of Education’s website about a coding error on the College Scorecard’s loan repayment rate metric that ED deemed “modest.” I frantically started working through the updated data…and the error wasn’t modest. (And according to one report, the error was discovered back in August 2016.) It turns out that the percentage of students listed as repaying at least $1 on principal on their loans dropped by between ten and 20 percentage points after fixing the error. Instead of agreeing this error was modest, I told the Wall Street Journal this represented a “quality control issue” that needed to be fixed going forward.

(3) The NCAA and SACS both failed to hold the University of North Carolina truly accountable for a fake classes scandal. The University of North Carolina at Chapel Hill has received well-deserved negative publicity for somehow allowing student-athletes (and some enterprising fraternity brothers) to take phony classes in the African-American studies program for almost 20 years. In October, the NCAA found there was no evidence it violated their policies because non-athletes also took the fake classes (and because colleges can set their own definitions of academic fraud). So surely SACS (UNC’s accreditor) would step in, right? SACS did put UNC on probation in 2015, but then lifted the sanctions after one year (even as some SACS members wanted to terminate UNC’s accreditation). But then UNC apparently made statements to the NCAA in 2017 that violated its agreement with SACS to not count any credits from the fake classes, briefly leading SACS to reconsider UNC’s statements in November. Within a week, SACS apologized for seeming to open a new investigation into UNC, so the university is officially off the hook for the scandal.

(2) Senate majority leader Mitch McConnell tried to protect one of his state’s community colleges from facing cohort default rate sanctions. Policymakers and oversight bodies like to talk about holding colleges accountable for their performance, but these same people tend to back off considerably when a college’s funding is actually hanging in the balance. This is particularly true when a college is a constituent—whether of an accrediting agency (see UNC above) or of a member of Congress. Cohort default rates (for which colleges can lose all federal financial aid if their rates cross a certain threshold) are a great example. The Obama administration let a number of colleges pass in 2014 by making controversial changes to how certain loans with multiple servicers were treated. Senate Majority Leader Mitch McConnell (R-KY) went even farther by adding language to an appropriations bill that would allow one community college in his state to avoid sanctions (and not apply to any other colleges). This is why all-or-nothing accountability systems rarely work as well as designers think they will.

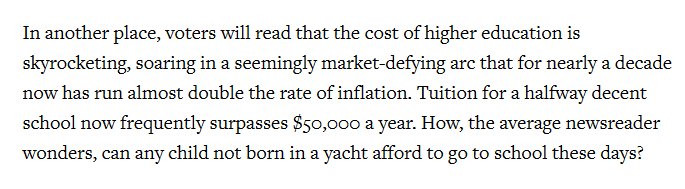

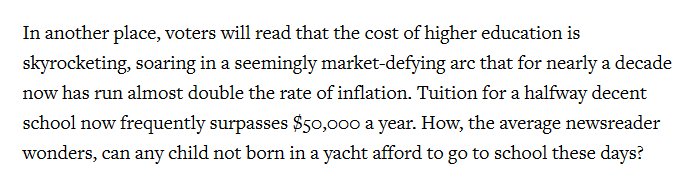

(1) Only “halfway decent” colleges have tuition above $50,000 per year. The rest of us might as well shut down right now. Some years, it’s hard to pick a standout event to top the year’s not top ten list. This year’s decision was obvious as soon as I made the mistake of clicking on this woeful piece from the Rolling Stone (which apparently still has fact-checking issues) called “The Great College Loan Swindle.” The Bard College alumnus who wrote the piece included this lovely snippet.

As soon as I got to that part of the piece, I stopped reading. If all public universities and most of private nonprofit higher education is garbage, then why am I a professor again?

As soon as I got to that part of the piece, I stopped reading. If all public universities and most of private nonprofit higher education is garbage, then why am I a professor again?

(Dis)honorable mentions (athletics division): Dartmouth football assistant coach punches out a window in Harvard’s press box, Oregon football assistant coach collects $63,750 for one day of work after being arrested for a DUI, Kentucky basketball fans send death threats to a referee following a close loss, three UCLA basketball players are lucky to not be in a Chinese jail after a shoplifting arrest (plus a bizarre feud between LaVar Ball and Donald Trump), colleges offering athletic scholarships to preteens, football coach heads to third job in 12 months (without sitting out a year like most players must).

(Dis)honorable mentions (non-athletics division): Allowing your university Twitter account to be hacked with profane messages, higher ed official claiming that genetics contribute to pay disparities by gender, selectively showing results to support an advocacy agenda, passing off descriptive statistics as causal research, typos of “casual inference” and “pubic education” abounding in published research.

With this post now being online, I’m planning to take a hiatus from blogging over the holiday season (unless something monumental happens in the higher education policy arena). I’ll see you all again in January—and if you can’t get enough of my takes on higher education, pre-order my book Higher Education Accountability for shipment in January. (Use promo code HDPD to get 30% off from Johns Hopkins University Press!)

A previous version of this post incorrectly referred to Debasish Dutta as the president of Rutgers University. He is in fact the chancellor of Rutgers-New Brunswick. The error has been corrected.

Much of Denisa’s research has examined state performance funding policies in higher education, which have spread throughout much of the country in the last two decades in spite of (to this point, at least) generally having at most very modest effects. In an article recently published in The Journal of Higher Education, Denisa worked with Jennifer Rippner of the University System of Georgia and Erik Ness of the University of Georgia to interview stakeholders in three states to learn more about how national organizations have helped to foster the spread of performance funding.

Much of Denisa’s research has examined state performance funding policies in higher education, which have spread throughout much of the country in the last two decades in spite of (to this point, at least) generally having at most very modest effects. In an article recently published in The Journal of Higher Education, Denisa worked with Jennifer Rippner of the University System of Georgia and Erik Ness of the University of Georgia to interview stakeholders in three states to learn more about how national organizations have helped to foster the spread of performance funding.